ARTICLE AD BOX

The Trump administration will end the last piece of pandemic-era student loan relief and send defaulted student loans to collections starting May 5.

This comes after President Donald Trump paused student loan repayment due to the COVID-19 pandemic in March 2020. President Joe Biden went on to extend this relief, and student loan repayments didn’t resume until October 2023. Even then, borrowers still weren’t penalized for late payments until last fall.

Now, the estimated 5 million people with federal student loans in default could see their wages garnished and their federal payments reduced as their loans are sent to collections.

Here’s what you need to know about your defaulted student loans:

How do I know if my loans are in default?

Defaulted student loans begin with delinquency, which happens when you miss a payment. After 90 days, this is reported to national credit bureaus, impacting your credit score.

Your loans will go into default if you haven’t made a payment in 270 days and haven’t made an agreement with your borrower, such as deferment or forbearance.

You can log into your federal student loan account to check the status of your loans.

I have loans in default. What happens now?

The Education Department will begin forced recollections on May 5.

That means the agency can garnish portions of your wages to pay the loans without a court order. Your credit score could also suffer, impacting your ability to obtain new loans or rent an apartment.

Officials could also withhold any tax refunds or other federal payments to put towards your loan payment. This could also mean withholding up to 15 percent of your monthly Social Security retirement and disability benefits.

If your loans are in default, the Federal Student Aid office will reach out in the coming weeks with information about the Default Resolution Group. The office can help you navigate your defaulted student loans.

How do I get out of default?

One option is to pay your loans off in full right away — but that isn’t feasible for most of the 5 million people in default.

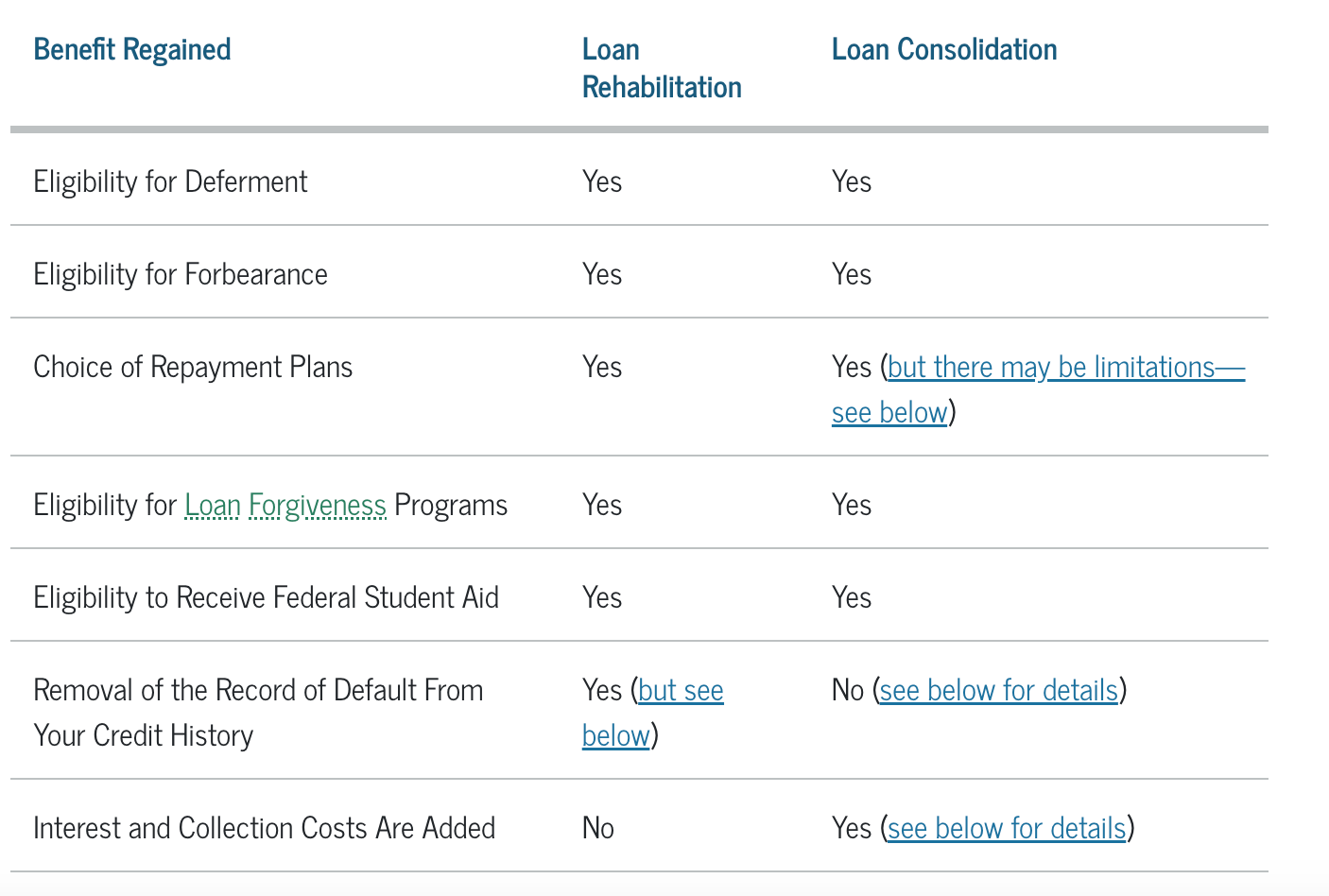

The two main options are rehabilitating your loans and consolidating your loans, according to the Federal Student Aid office.

Rehabilitating your loan means that you agree in writing to make nine reasonable monthly payments, which are determined by the loan holder, within 20 days of the due date. You must also make all nine payments over 10 consecutive months.

Depending on your income, your monthly payment under a rehabilitation plan could be as low as $5.

Consolidating your loan allows you to pay off one or multiple federal student loans with a new consolidation loan. To consolidate, you can agree to repay the new loan under an income-driven repayment plan. Alternatively, you can make three consecutive, voluntary, on-time and full monthly payments on the defaulted loan before you consolidate it.

You can learn more about reconciliation and consolidation from the Federal Student Aid office.

What is loan deferment?

Your loan may be eligible for deferment, which means you don’t have to make payments. This also means you aren’t making any progress toward repaying your loan.

If you’re enrolled in college or a career school at least half-time, your loans are automatically in deferment.

However, there are various other reasons for deferment, including cancer treatment, economic hardship, graduate fellowship completion, military service, and unemployment.

Learn more about deferment from the Federal Student Aid office.

English (US) ·

English (US) ·